Spend controls

Real-time transaction decisioning that puts you in control.

Spend controls give you the flexibility to create sophisticated, policy-aligned rules for approving or declining card transactions in real time. You define the logic, we enforce it reliably, securely, and at scale.

Fully managed, high-performance platform

Our platform is built to simplify complexity. You only need to define the rules and assign them to cards. We take care of rule execution, system availability, scalability, and integration with the card schemes. With consistently fast response times and excellent uptime, your users can count on seamless purchases at the point of sale.

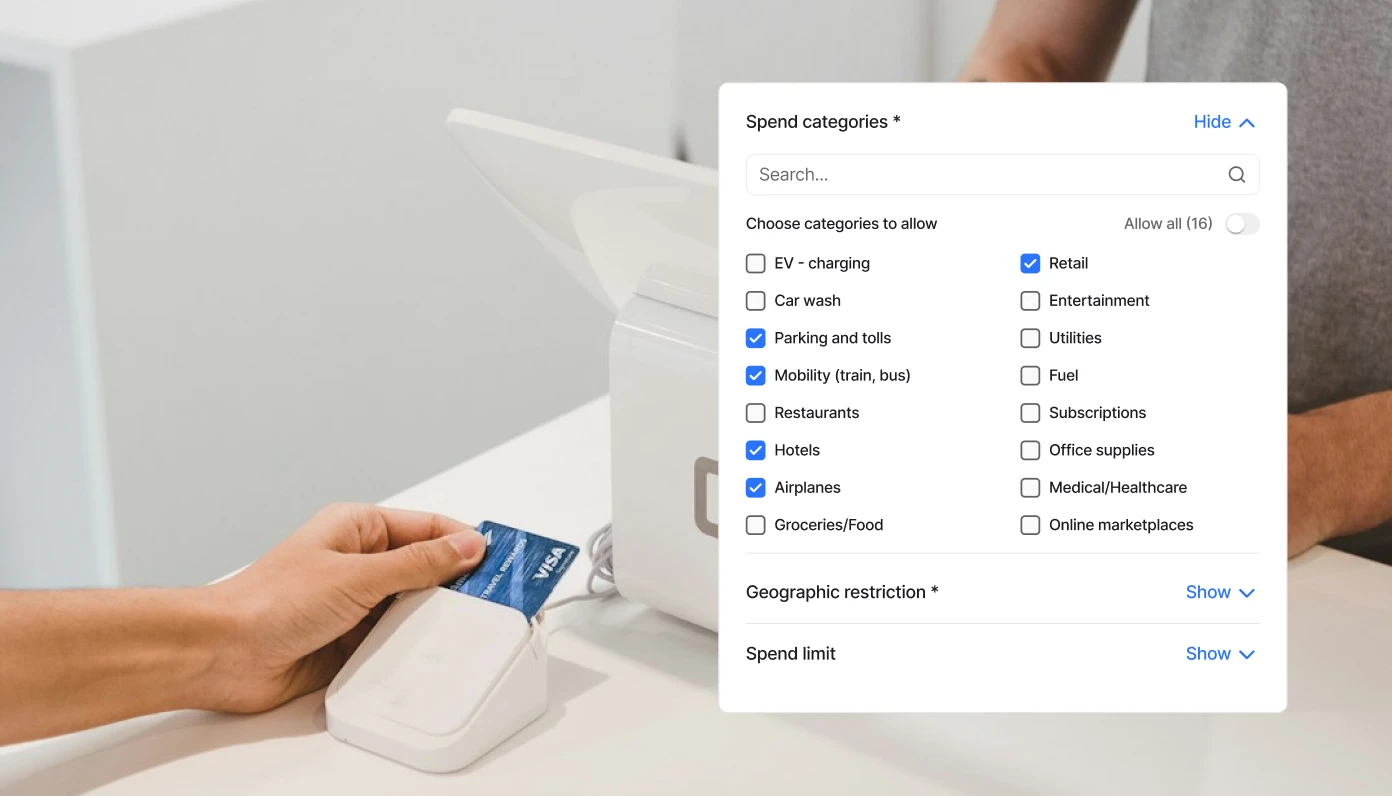

Benefits of spend controls

- Create tailored card experiences: Support niche use cases like lunch cards, employee expense limits, or merchant-specific gift cards with fine-grained control.

- Reduce fraud and misuse: Mynt's limits on geography, merchant category, or even specific merchants to reduce the risk of inappropriate or fraudulent use.

- Drive customer loyalty: Deliver differentiated, custom-fit card products that competitors can’t easily replicate.

How it works

Spend control rules are enforced at the moment of authorisation. When a card is used, the transaction message is evaluated against the rule set in real time. If the rule conditions are met, the transaction is either approved or declined based on your configuration.

Authorisation messages include data such as merchant category code, country, transaction amount, terminal type, and more. These inputs form the basis for powerful, context-aware controls.

Rule types and parameters

Spend controls are composed of rules, each evaluating transaction parameters. Rules can be simple (if X then decline) or combined (if X and Y then decline).

Rule parameters

All rules are based on data included in the authorisation message, such as:

- Merchant category code (MCC)

- Merchant ID

- Merchant country

- Transaction amount

- Currency

- Contactless / chip / online

- Point of sale terminal type

- Time and date

Note: The availability and accuracy of this data depends on the merchant and the card scheme. While most merchants follow standard definitions, edge cases or inconsistencies may occur.

Merchant category code

Limit card usage to specific types of merchants using MCCs. Ideal for general category-level control. Examples:

- Lunch cards: Limit to MCC 5812, 5814 (restaurants and fast food)

- Mobility cards: MCC 4111, 4112, 4131 (public transport)

- Fuel & EV: MCC 5541, 5542, 5552 (fuel stations, EV chargers)

Specific merchants

Create allow-lists or block-lists based on merchant identifiers when MCCs are too broad or imprecise.

Examples:

- Gift cards tied to a single store

- Limited network cards for a specific retail chain

- E-commerce single-use cards tied to a specific merchant

Note: Since there's no global merchant directory, merchant IDs must be gathered from transactions or supplied by the merchant.

Merchant country

Control where in the world a card can be used. These rules are often used to support local policies or mitigate risk.

Examples:

- Domestic-only cards for local contractors

- Blocking cards in high-risk or sanctioned countries (note: Mynt’s fraud controls enforce mandatory country blocks which cannot be overridden)