Native integration

Card partner API - native integration

The Native integration is quite different in that the partner builds more of the functionality into their own interfaces (web and/or mobile). Company's admin person will onboard in the partner's interface, but will complete the KYC and credit application steps using free-standing mynt modules. Cards are ordered by the partner via API, and users activate their physical cards in the partner's interface (generally the mobile app)(virtual cards are instantly active once ordered). PIN codes and sensitive card information are also presented in the partner's interface, and therefore places higher requirements on security (Strong Customer Authentication (SCA)). Partner must build functionality and workflows to support provisioning of tokenization in app (ApplePay and GooglePay), if these are in scope. Tokenization requires correct telephone number on user entities.

Once a card has been activated, the card holder can start making purchases given that there's an amount available to spend (either client funds or Mynt credit). Purchases are pushed to the partner via the transaction webhook. See the transaction data model for a summary of parameters. Partner must adapt their company interface and workflow to handle pushed card transactions. Note that 3Ds purchases must be approved by the user in the partner app when they arise, and such approvals must be relayed to Mynt.

KYC and credit modules

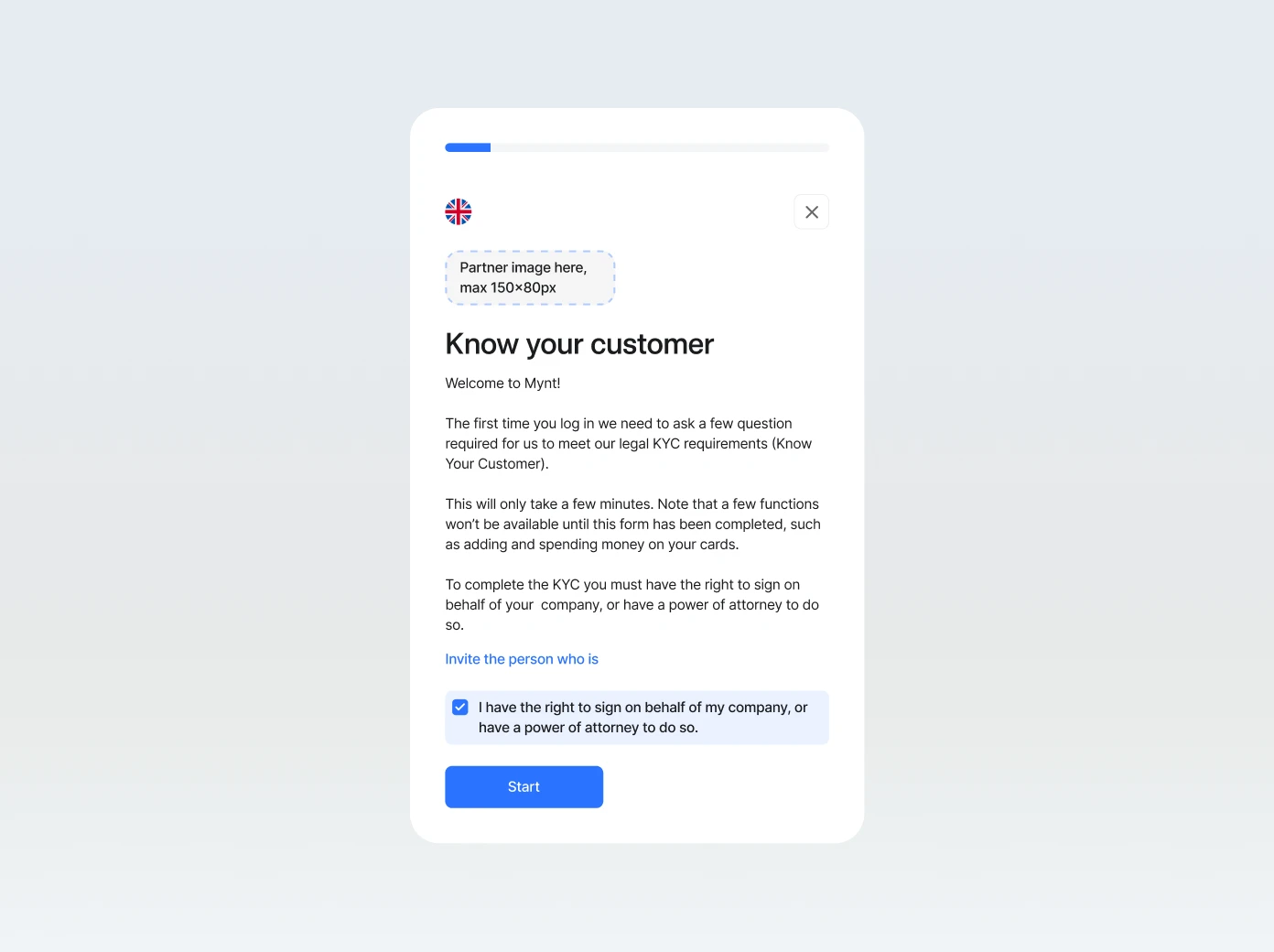

The Mynt modules for KYC and credit application are free-standing in the sense that they are provided by URLs, which the partner must present to the company admin person. It is helpful if the admin can either trigger the flows directly (open in new tab) or is presented with the ability to send the link by email to the appropriate person in the company. Note that the KYC must be answered by a company signatory or other authorized person (with power of attorney from a signatory).

Mynt will not send any notifications to the company directly, but these events are provided via webhooks. Credit invoices and reminders are always sent by Mynt directly. Credit invoices and topup receipts are sent to the partner via webhooks, including reference to PDF document, so that these can be handled appropriately in an accounting context.

Partner must implement Mynt's controls on product level (ENABLED, DISABLED), and credit feature (ENABLED, DISABLED). If the company level approval is DISABLED the product cannot be offered to the company. This can happen for example if there is risk of money laundering that has been discovered, or Mynt for any reason cannot provide the product to the company. Credit feature can be DISABLED if Mynt for any reason can't provide credit to the company.

Mynt provides endpoints for the current state for KYC process (NOT_STARTED, PENDING, APPROVED), credit application process. These are helpful to show to the company in the interface. Note that KYC denied state will also result in product being DISABLED. In the case the company is denied, Mynt will handle the communication directly with the company according to legal requirements.